| the_enron_scandal_tobias_pavel_mylene_encontro_2012.pdf |

|

0 Comments

A larger organization can convert its accounts receivable into cash at once by securitizing the receivables. This means that individual receivables are aggregated into a new security, which is then sold as an investment instrument. A securitization can result in an extremely low interest rate for the issuing entity, since the securities are backed by a liquid form of collateral (i.e., receivables). In essence, a receivables securitization is accomplished with these steps:

These process steps indicate that the securitization of accounts receivable is complex, and so is reserved for only larger companies that can attend to the many steps. Also, the receivables included in a pool should be widely differentiated (so there are many customers), with a low historical record of customer defaults. Despite the complexity, securitization is tempting for the following reasons:

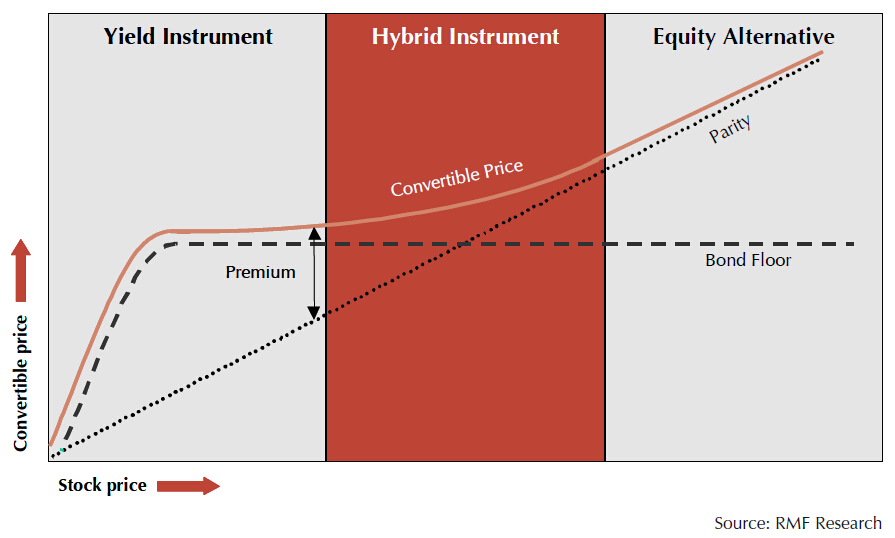

Convertible Bonds (CBs) are fixed income instruments that can be converted into a fixed number of shares of the issuer at the option of the investor. Bonds that are convertible into shares other than the issuer’s are called exchangeable bonds.

Convertibles are fascinating hybrid securities. On the one hand, they have the benefits of debt instruments that pay fixed coupons and will be redeemed at maturity at a pre-specified price. On the other hand, the embedded conversion option provides the investor with a participation in the upside potential of the underlying equity. The conversion right provides the bond holder with a better-of-two-choices option. At maturity, the Convertible Bonds are worth the higher of (a) their redemption value (the price at which the issuer had agreed to buy the bonds back) or (b) the market value of the underlying shares. In other words, a Convertible Bond is a straight bond with an embedded equity call option. Due to this call option, the Convertible will participate in any increase of the underlying equity, while the fixed income portion provides capital protection, should the share price fall.

The IPO market has undergone a sea change. We as investors can only sit back and remember the days of under priced IPO’s in the Controller of Capital issue days-where getting allotment was akin to winning a lottery. Then came the era of free pricing-when many an over priced issue hit the market , still there were some pearls to be found as suddenly some sectors got re rated by the market and the price of the issues seemed reasonable. Then in 1998 Securities and Exchange Board of India (SEBI) allowed every issuer of equity shares of Rs 250 million and above to have an option to make an issue through the Book Building Process. The age of the big boys had arrived-the small investor’s role in the IPO market was to get marginalised. Book Building refers to the collection of bids from investors, which is based on an indicative price range, the issue price being fixed after the bid closing date. The principal intermediaries involved in a book building process are the company, Book Running Lead Manager (BRLM) and syndicate members who are intermediaries registered with SEBI and eligible to act as underwriters. Syndicate members are appointed by the BRLM. The book building process is undertaken basically to determine investor appetite for a share at a particular price. It is undertaken before making a public offer and it helps determine the issue price and the number of shares to be issued. The process begins with consultations between issuer company, the fund managers and the institutional investors. The above process is used to derive a price-band with a median point at which the demand for the company’s stock is maximum. The issuer company, in tandem with the lead manager and the book runner, then fixes a price band for the issue. The investor is informed of the price band and he then bids at a price he thinks appropriate. The bidding is done just like an open auction. The bidding period is kept open for at least five working days. The advertisement announcing the bidding contains the date of the opening of the offer and the closing date. The issue document contains the name of syndicate members who are entitled to receive the bids. Even the offer document contains the conditions of accepting the bids and the procedure of bidding. The bidding centers are electronically connected to maintain transparency and also eliminate the time lag between making and receiving of the bid. Individual and institutional investors have to place their bids only through the ‘syndicate members’ who have the right to vet the bids. The bids can be revised innumerable number of times before the issue closes. To maintain transparency in the bidding process, at the end of every bidding session the demand for the issue is shown in the graph format on the terminals. Once the company gets various bids from the investor, it decides the final price at which it is willing to issue the stock. Since the company has already decided the quantum of funds it wants to raise it finalizes the number of shares it will now issue at the price fixed. The issue price for the placement portion and offer to the public shall be the same. As per the SEBI rules known to everyone, a company going public has to offer its minimum 25 per cent of issued post-issue equity to the public and maximum of 75 per cent post issue equity can remain with the promoters. However, by a recent amendment large software companies making an issue of over Rs.200 crores (including premium) need offer only a minimum of 10 per cent of post issue equity. Out of the total public issue size, 90 per cent of the issue can be offered through book building process while only 10 per cent of the issue can be offered via fixed price portion. Out of the book building portion, a minimum of 10 per cent of the issue size has to be reserved for retail bidders while 75 per cent of the issue can be offered to wholesale bidders. A retail investor in book building process is an investor who has to bid for a minimum of 100 equity shares and in multiples of 50 equity shares thereafter subject to a maximum of 2000 equity shares. In case of wholesale bidders the bid has to for a minimum of 500 equity shares and in multiples of 50 equity shares thereafter. In case of over-subscription in the retail category, allocation will be made on a proportionate basis and in consultation with the regional stock exchange. In case of balance book-built portion the same shall be available to wholesale bidders and the company in consultation with the Allocation Committee has the discretion to allocate to any of the investors, who have bid, at or above the issue price in wholesale bidder category. While bidding for the equity shares of the company in a book built portion, each bidder shall, with the submission of the bid-cum-application form, draw a cheque/demand draft/stockinvest for the maximum amount of this bid in favor of the escrow account of the escrow collection bank. Bid form accompanied by cash is not accepted. However, the syndicate member(s) at their discretion may waive such requirement of payment at the time of submission of the did form for wholesale bidders. Where such payment at the time of bidding is waived at the discretion of the syndicate member or where there is a shortfall as a result of cut-off price being more than highest price in the indicative price band, the issue price or the difference, as the case may be would be paid, favoring the escrow account within 4 days on communication by the BRLM of the list of bidders who have been allocated equity shares to the syndicate members. As a result of the book building process , by merely offering 6.25 per cent of the post issue equity, the shares of the company can get listed on the major stock exchanges like NSE and BSE. Here, after listing, due to low floating stock, it becomes very easy for the vested interests to manipulate the price. Also, out of 18.75 per cent of the post issue equity, reserved for wholesale bidders, the said shares are conveniently allotted by the company and BRLM to persons of their choice and selection. Ironically, these allottees can get the allotment of shares without paying a single penny along with their bids. Due to these flaws and inadequate provisions, SEBI has thought of streamlining book building norms and it was decided that to avoid conflict of interests during book-building and maintain the integrity of the process and an arms-length relationship between those involved in book building and their associates. Though still a new concept, book building is here to stay and represents a capital market which is in the process of maturing. (Note: This article is from http://www.karvy.com/articles/bookbuilding.htm)

|

|||||||||