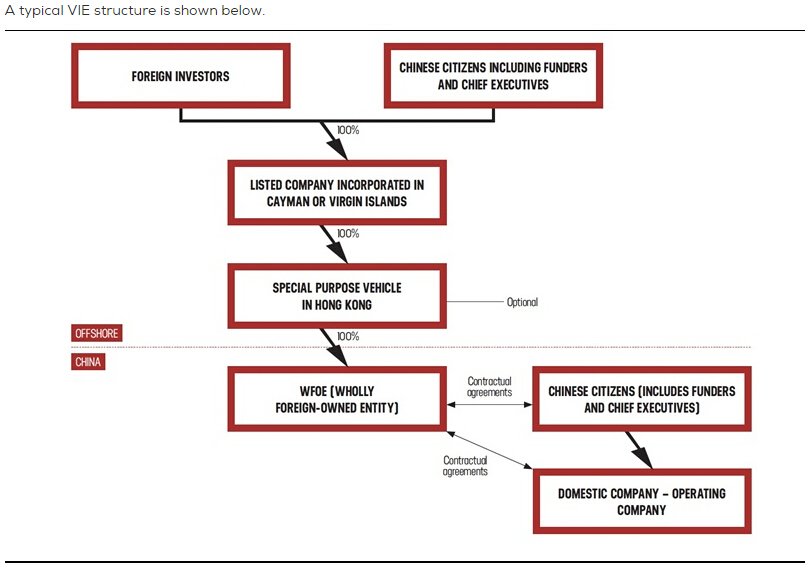

The VIE structure (协议控股) was developed in the late 1990s. Arguably, it’s a workaround for Chinese companies that operate in sensitive industries where foreign direct investment is restricted or prohibited. In the wake of the Enron collapse, the US required public companies to consolidate off balance sheet structures. China companies quickly realized that they could use the post-Enron rules – specifically FIN 46 – to consolidate operating businesses that China law prohibited foreigners to own (e.g., internet businesses). This consolidation was highly desirable for IPOs. Just under half of all Chinese companies on the NASDAQ and NYSE currently use this structure.

In Alibaba’s filing with the US Stock Exchange Commission (SEC), Alibaba stated that the company’s licences/permits to operate websites in China are held by its Variable Interest Entities (VIEs). The VIEs are 100% owned by Chinese citizens, more specifically the funders and the chairman of the board, Jack Yun Ma.

In other words, Alibaba Group Holding Ltd doesn’t have any direct ownership of critical elements of its businesses such as the statutory licences/permits in China, and the main network operation systems. The listed company will have effective control over its VIEs through complicated contractual agreements.

For more detailed explanation for VIEs see China Accounting Blog

In Alibaba’s filing with the US Stock Exchange Commission (SEC), Alibaba stated that the company’s licences/permits to operate websites in China are held by its Variable Interest Entities (VIEs). The VIEs are 100% owned by Chinese citizens, more specifically the funders and the chairman of the board, Jack Yun Ma.

In other words, Alibaba Group Holding Ltd doesn’t have any direct ownership of critical elements of its businesses such as the statutory licences/permits in China, and the main network operation systems. The listed company will have effective control over its VIEs through complicated contractual agreements.

For more detailed explanation for VIEs see China Accounting Blog